HFT回测进阶1: 环境准备

source: wtcpp/folder01/file02.md

Tip

请使用最新版0.9dev源码(20220303)

准备数据

- 参考文章"数据压缩/解压"准备自己的数据(包括bar级csv数据和tick级dsb数据)

- 本文自己准备的数据(外汇数据, 假设交易所: CUSTOM, 品种: FX, 合约名称: EURUSD, 1分钟csv数据, tick级dsb数据)

准备配置文件

1. 配置文件

- logcfgbt.yaml

- configbt.yaml

- storage(数据目录)

- bin(压缩数据, tick回放使用)

- ticks(tick数据每天一个文件,起名要按固定格式)

- CUSTOM.FX.EURUSD_tick_20220221.dsb

- CUSTOM.FX.EURUSD_tick_20220222.dsb

- CUSTOM.FX.EURUSD_tick_20220223.dsb

- ticks(tick数据每天一个文件,起名要按固定格式)

- csv(csv数据, bar回放使用, 文件名固定格式)

- CUSTOM.FX.EURUSD_m1

- bin(压缩数据, tick回放使用)

- common(配置目录)

- commodities.json"

- contracts.json"

- fees.json"

- holidays.json"

- sessions.json"

configbt.yaml 样式

# 回测参数

replayer:

basefiles:

commodity: ./common/commodities.json

contract: ./common/contracts.json

holiday: ./common/holidays.json

session: ./common/sessions.json

mode: csv # 回测模式, 可自动加载csv文件下的bar数据

path: ./storage/

fees: ./common/fees.json

stime: 202202210800 # tick回测一天数据量足够测试了

etime: 202202220900

tick: true # 使用tick数据, 如果为false, 会自动生成模拟tick数据

env:

mocker: hft # 模式

slippage: 5 # 滑点

hft:

error_rate: 30

# 策略工厂dll文件名称

module: WtHftStraFact

# 策略配置

strategy:

id: hft_id

# 策略名称(在策略工厂源码中有用)

name: HftDemoStrategy

# 策略参数

params:

code: CUSTOM.FX.EURUSD

count: 6

second: 5

freq: 20

offset: 0

reserve: 0

stock: false

use_newpx: true

logcfgbt.yaml

dyn_pattern:

strategy:

async: false

level: debug

sinks:

- filename: BtLogs/Strategy/%s.log

pattern: '[%Y.%m.%d %H:%M:%S - %-5l] %v'

truncate: true

type: basic_file_sink

root:

async: false

level: debug

sinks:

- filename: BtLogs/BtRunner.log

pattern: '[%Y.%m.%d %H:%M:%S,%F - %-5l] %v'

truncate: true

type: basic_file_sink

- pattern: '[%m.%d %H:%M:%S - %^%-5l%$] %v'

type: console_sink

Tip

以下配置都是根据个人情况自定义配置的

commodities.json

{

"CUSTOM": {

"FX": {

"covermode": 0,

"pricemode": 0,

"category": 1,

"precision": 5,

"pricetick": 0.00001,

"volscale": 500,

"name": "外汇",

"exchg": "CUSTOM",

"session": "ALLDAY",

"holiday": "USD"

}

}

}

contracts.json

{

"CUSTOM": {

"EURUSD": {

"name": "欧元兑美元",

"code": "EURUSD",

"exchg": "CUSTOM",

"product": "FX",

"maxlimitqty": 20,

"maxmarketqty": 10

}

}

}

fees.json

{

"CUSTOM.FX":

{

"open":0.00023,

"close":0.00023,

"closetoday":0.0,

"byvolume":true

}

}

holidays.json

{

"USD" : [20210212,20210215,20210216,20210217,20210405,20210503,20210504,20210505,20210614,20210920,20210921,20211001,20211004,20211005,20211006,20211007]

}

sessions.json

{

"ALLDAY":{

"name":"全天候盘",

"offset": -480,

"sections":[

{

"from": 800,

"to": 800

}

]

}

}

准备策略

1.为了方便回测, 建议修改策略文件 WtHftStraDemo.cpp , 主要是在策略中添加一些日志输出信息, 方便调试. 这里就直接给源码, 不再解释(主要添加了 _ctx->stra_log_info... )

#include "WtHftStraDemo.h"

#include "../Includes/IHftStraCtx.h"

#include "../Includes/WTSVariant.hpp"

#include "../Includes/WTSDataDef.hpp"

#include "../Includes/WTSContractInfo.hpp"

#include "../Share/TimeUtils.hpp"

#include "../Share/decimal.h"

#include "../Share/fmtlib.h"

extern const char* FACT_NAME;

WtHftStraDemo::WtHftStraDemo(const char* id)

: HftStrategy(id)

, _last_tick(NULL)

, _last_entry_time(UINT64_MAX)

, _channel_ready(false)

, _last_calc_time(0)

, _stock(false)

, _unit(1)

, _cancel_cnt(0)

, _reserved(0)

{

}

WtHftStraDemo::~WtHftStraDemo()

{

if (_last_tick)

_last_tick->release();

}

const char* WtHftStraDemo::getName()

{

return "HftDemoStrategy";

}

const char* WtHftStraDemo::getFactName()

{

return FACT_NAME;

}

bool WtHftStraDemo::init(WTSVariant* cfg)

{

//这里演示一下外部传入参数的获取

_code = cfg->getCString("code");

_secs = cfg->getUInt32("second");

_freq = cfg->getUInt32("freq");

_offset = cfg->getUInt32("offset");

_reserved = cfg->getDouble("reserve");

_stock = cfg->getBoolean("stock");

_unit = _stock ? 100 : 1;

return true;

}

void WtHftStraDemo::on_entrust(uint32_t localid, bool bSuccess, const char* message, const char* userTag)

{

}

void WtHftStraDemo::on_init(IHftStraCtx* ctx)

{

WTSTickSlice* ticks = ctx->stra_get_ticks(_code.c_str(), 30);

if (ticks)

ticks->release();

WTSKlineSlice* kline = ctx->stra_get_bars(_code.c_str(), "m1", 30);

if (kline)

kline->release();

ctx->stra_sub_ticks(_code.c_str());

_ctx = ctx;

_ctx->stra_log_info("策略回调 on_init");

}

void WtHftStraDemo::on_tick(IHftStraCtx* ctx, const char* code, WTSTickData* newTick)

{

// newTick是类, actiontime是毫秒要/1000

_ctx->stra_log_info(fmt::format("策略回调 on_tick. date: {}, time: {}, open: {}", newTick->actiondate(), newTick->actiontime()/1000, newTick->open()).c_str());

if (_code.compare(code) != 0)

return;

if (!_orders.empty())

{

check_orders();

return;

}

if (!_channel_ready)

return;

WTSTickData* curTick = ctx->stra_get_last_tick(code);

if (curTick)

curTick->release();

uint32_t curMin = newTick->actiontime() / 100000; //actiontime是带毫秒的,要取得分钟,则需要除以10w

if (curMin > _last_calc_time)

{//如果spread上次计算的时候小于当前分钟,则重算spread

//WTSKlineSlice* kline = ctx->stra_get_bars(code, "m5", 30);

//if (kline)

// kline->release();

//重算晚了以后,更新计算时间

_last_calc_time = curMin;

}

//30秒内不重复计算

uint64_t now = TimeUtils::makeTime(ctx->stra_get_date(), ctx->stra_get_time() * 100000 + ctx->stra_get_secs());//(uint64_t)ctx->stra_get_date()*1000000000 + (uint64_t)ctx->stra_get_time()*100000 + ctx->stra_get_secs();

if(now - _last_entry_time <= _freq * 1000)

{

return;

}

int32_t signal = 0;

double price = newTick->price();

//计算部分

double pxInThry = (newTick->bidprice(0)*newTick->askqty(0) + newTick->askprice(0)*newTick->bidqty(0)) / (newTick->bidqty(0) + newTick->askqty(0));

//理论价格大于最新价

if (pxInThry > price)

{

//正向信号

signal = 1;

}

else if (pxInThry < price)

{

//反向信号

signal = -1;

}

if (signal != 0)

{

double curPos = ctx->stra_get_position(code);

curPos -= _reserved;

WTSCommodityInfo* cInfo = ctx->stra_get_comminfo(code);

if(signal > 0 && curPos <= 0)

{//正向信号,且当前仓位小于等于0

//最新价+2跳下单

double targetPx = price + cInfo->getPriceTick() * _offset;

auto ids = ctx->stra_buy(code, targetPx, _unit, "enterlong");

_mtx_ords.lock();

for( auto localid : ids)

{

_orders.insert(localid);

}

_mtx_ords.unlock();

_last_entry_time = now;

}

else if (signal < 0 && (curPos > 0 || ((!_stock || !decimal::eq(_reserved,0)) && curPos == 0)))

{//反向信号,且当前仓位大于0,或者仓位为0但不是股票,或者仓位为0但是基础仓位有修正

//最新价-2跳下单

double targetPx = price - cInfo->getPriceTick()*_offset;

auto ids = ctx->stra_sell(code, targetPx, _unit, "entershort");

_mtx_ords.lock();

for (auto localid : ids)

{

_orders.insert(localid);

}

_mtx_ords.unlock();

_last_entry_time = now;

}

}

}

void WtHftStraDemo::check_orders()

{

if (!_orders.empty() && _last_entry_time != UINT64_MAX)

{

uint64_t now = TimeUtils::makeTime(_ctx->stra_get_date(), _ctx->stra_get_time() * 100000 + _ctx->stra_get_secs());

if (now - _last_entry_time >= _secs * 1000) //如果超过一定时间没有成交完,则撤销

{

_mtx_ords.lock();

for (auto localid : _orders)

{

_ctx->stra_cancel(localid);

_cancel_cnt++;

_ctx->stra_log_info(fmt::format("Order expired, cancelcnt updated to {}", _cancel_cnt).c_str());

}

_mtx_ords.unlock();

}

}

}

void WtHftStraDemo::on_bar(IHftStraCtx* ctx, const char* code, const char* period, uint32_t times, WTSBarStruct* newBar)

{

uint32_t barTime = (uint32_t)(newBar->time % 10000 * 100);

_ctx->stra_log_info(fmt::format("策略回调 on_bar. date: {}, time: {}, open: {}", newBar->date, barTime, newBar->open).c_str());

}

void WtHftStraDemo::on_trade(IHftStraCtx* ctx, uint32_t localid, const char* stdCode, bool isBuy, double qty, double price, const char* userTag)

{

_ctx->stra_log_info("策略回调 on_trade");

}

void WtHftStraDemo::on_position(IHftStraCtx* ctx, const char* stdCode, bool isLong, double prevol, double preavail, double newvol, double newavail)

{

_ctx->stra_log_info("策略回调 on_position");

}

void WtHftStraDemo::on_order(IHftStraCtx* ctx, uint32_t localid, const char* stdCode, bool isBuy, double totalQty, double leftQty, double price, bool isCanceled, const char* userTag)

{

_ctx->stra_log_info("策略回调 on_order");

//如果不是我发出去的订单,我就不管了

auto it = _orders.find(localid);

if (it == _orders.end())

return;

//如果已撤销或者剩余数量为0,则清除掉原有的id记录

if(isCanceled || leftQty == 0)

{

_mtx_ords.lock();

_orders.erase(it);

if (_cancel_cnt > 0)

{

_cancel_cnt--;

_ctx->stra_log_info(fmt::format("cancelcnt -> {}", _cancel_cnt).c_str());

}

_mtx_ords.unlock();

}

}

void WtHftStraDemo::on_channel_ready(IHftStraCtx* ctx)

{

_ctx->stra_log_info("策略回调 on_channel_ready");

double undone = _ctx->stra_get_undone(_code.c_str());

if (!decimal::eq(undone, 0) && _orders.empty())

{

//这说明有未完成单不在监控之中,先撤掉

_ctx->stra_log_info(fmt::format("{}有不在管理中的未完成单 {} 手,全部撤销", _code, undone).c_str());

bool isBuy = (undone > 0);

OrderIDs ids = _ctx->stra_cancel(_code.c_str(), isBuy, undone);

for (auto localid : ids)

{

_orders.insert(localid);

}

_cancel_cnt += ids.size();

_ctx->stra_log_info(fmt::format("cancelcnt -> {}", _cancel_cnt).c_str());

}

_channel_ready = true;

}

void WtHftStraDemo::on_channel_lost(IHftStraCtx* ctx)

{

_ctx->stra_log_info("策略回调 on_channel_lost");

_channel_ready = false;

}

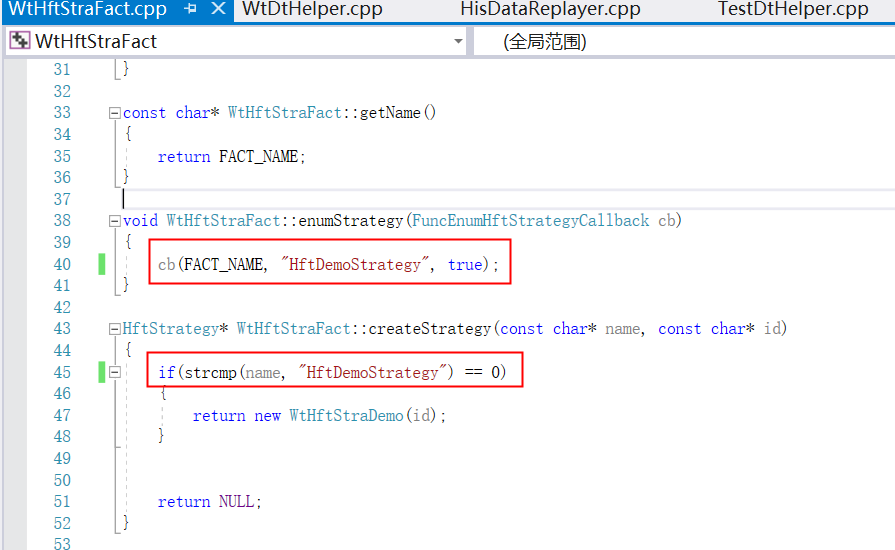

2.修改策略工厂文件 WtHftStraFact.cpp 或配置文件 configbt.yaml->strategy->name 字段  一定要保证上述两个位置和configbt.yaml中策略配置下的策略名称一致

一定要保证上述两个位置和configbt.yaml中策略配置下的策略名称一致

3.修改完毕后右键点击WtHftStraFact, 重新生成

4.将重新生成的Debug文件夹下 WtHftStraFact.dll 放到 WtBtRunner 文件夹下

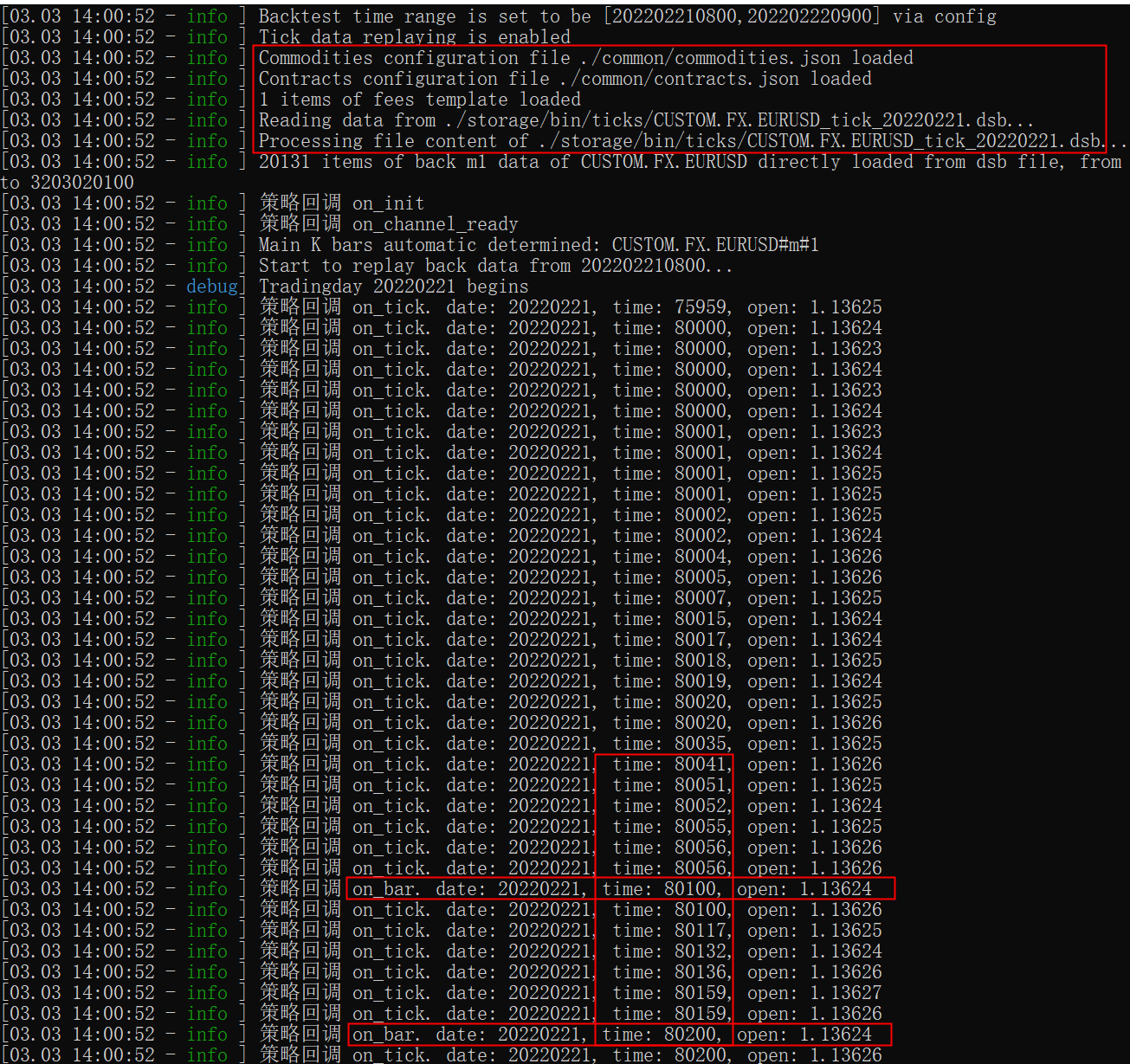

成功验证

执行 WtBtRunner 程序, 成功截图如下