CTA仿真进阶篇1: 环境部署

source: wtcpp/folder03/file06.md

相比HFT仿真, CTA的仿真更加复杂点, 因此我们之前先讲解了HFT仿真交易, 如果对此不熟悉的小伙伴建议看之前的文章. 只有熟悉了HFT仿真逻辑之后才能较容易理解CTA仿真逻辑.

本系列文章建立在你对WT项目已有一定了解的基础上. 我将会逐步探索CTA仿真交易的各个细节, 包括风控管理, 佣金配置, 执行器配置, 过滤器配置, 开平策略配置等. 因此对其他基础的配置包括文件加载等将会一笔带过.

启动数据落地程序

CTA仿真策略一般需要获取K线数据, 这就要求必须打开数据落地程序. (即接收交易所数据保存到本地, 并将数据广播到本地端口, 供其他程序使用)

其实有两个程序都可以实现这一功能, 一个是 QuoteFactory, 另一个是 TestDtPorter, 而 TestDtPorter 主要是方便上层调用的, 因此建议大家使用 QuoteFactory 打开数据落地程序.

文件配置

这里给出我使用的相关配置(7*24小时, openctp).

commodities.json

{

"CFFEX": {

"IC": {

"covermode": 0,

"pricemode": 0,

"category": 1,

"precision": 1,

"pricetick": 0.2,

"volscale": 200,

"name": "中证֤",

"exchg": "CFFEX",

"session": "TTS24",

"holiday": "CHINA"

},

"IF": {

"covermode": 0,

"pricemode": 0,

"category": 1,

"precision": 1,

"pricetick": 0.2,

"volscale": 300,

"name": "沪深",

"exchg": "CFFEX",

"session": "TTS24",

"holiday": "CHINA"

},

"IH": {

"covermode": 0,

"pricemode": 0,

"category": 1,

"precision": 1,

"pricetick": 0.2,

"volscale": 300,

"name": "上证",

"exchg": "CFFEX",

"session": "TTS24",

"holiday": "CHINA"

}

}

}

contracts.json

{

"CFFEX": {

"IC2203": {

"name": "中证2203",

"code": "IC2203",

"exchg": "CFFEX",

"product": "IC",

"maxlimitqty": 20,

"maxmarketqty": 10

},

"IC2206": {

"name": "中证֤2206",

"code": "IC2206",

"exchg": "CFFEX",

"product": "IC",

"maxlimitqty": 20,

"maxmarketqty": 10

},

"IC2209": {

"name": "中证֤2209",

"code": "IC2209",

"exchg": "CFFEX",

"product": "IC",

"maxlimitqty": 20,

"maxmarketqty": 10

},

"IF2203": {

"name": "沪深2203",

"code": "IF2203",

"exchg": "CFFEX",

"product": "IF",

"maxlimitqty": 20,

"maxmarketqty": 10

},

"IF2206": {

"name": "沪深2206",

"code": "IF2206",

"exchg": "CFFEX",

"product": "IF",

"maxlimitqty": 20,

"maxmarketqty": 10

},

"IF2209": {

"name": "沪深2209",

"code": "IF2209",

"exchg": "CFFEX",

"product": "IF",

"maxlimitqty": 20,

"maxmarketqty": 10

},

"IH2203": {

"name": "上证֤2203",

"code": "IH2203",

"exchg": "CFFEX",

"product": "IH",

"maxlimitqty": 20,

"maxmarketqty": 10

},

"IH2206": {

"name": "上证֤2206",

"code": "IH2206",

"exchg": "CFFEX",

"product": "IH",

"maxlimitqty": 20,

"maxmarketqty": 10

},

"IH2209": {

"name": "上证֤֤2209",

"code": "IH2209",

"exchg": "CFFEX",

"product": "IH",

"maxlimitqty": 20,

"maxmarketqty": 10

}

}

}

sessions.json

{

"TTS24":{

"name":"TTS24测试",

"offset": -480,

"auction":{

"from": 802,

"to": 803

},

"sections":[

{

"from": 803,

"to": 758

}

]

},

"ALLDAY":{

"name":"全天候盘",

"offset": -480,

"sections":[

{

"from": 800,

"to": 800

}

]

}

}

QFConfig.yaml

basefiles:

commodity: ./common/commodities.json

contract: ./common/contracts.json

holiday: ./common/holidays.json

session: ./common/sessions.json

broadcaster:

active: true

bport: 3997

broadcast:

- host: 255.255.255.255

port: 9001

type: 2

multicast_:

- host: 224.169.169.169

port: 9002

sendport: 8997

type: 0

- host: 224.169.169.169

port: 9003

sendport: 8998

type: 1

- host: 224.169.169.169

port: 9004

sendport: 8999

type: 2

allday: true # 使用全天候环境

parsers:

- active: true

broker:

id: tts24

module: ParserCTP

front: tcp://122.51.136.165:20004

localtime: true # 使用本地时间戳

ctpmodule: tts_thostmduserapi_se

pass: ******

user: ******

# code: SHFE.au2206,SHFE.au2208

filter: CFFEX

statemonitor: statemonitor.yaml

writer:

module: WtDataStorage

async: true

groupsize: 1000

path: ../Storage

savelog: false

这里提醒两点

QFConfig.yaml文件一个是启用了allday字段, 这样就可以避免状态机干扰测试环境- 在

parsers中启用了localtime字段, 这在使用openctp时是必须做的. writer中设置数据保存目录是../Storage, 这个必须和接下来的CTP仿真时数据读取目录保持一致

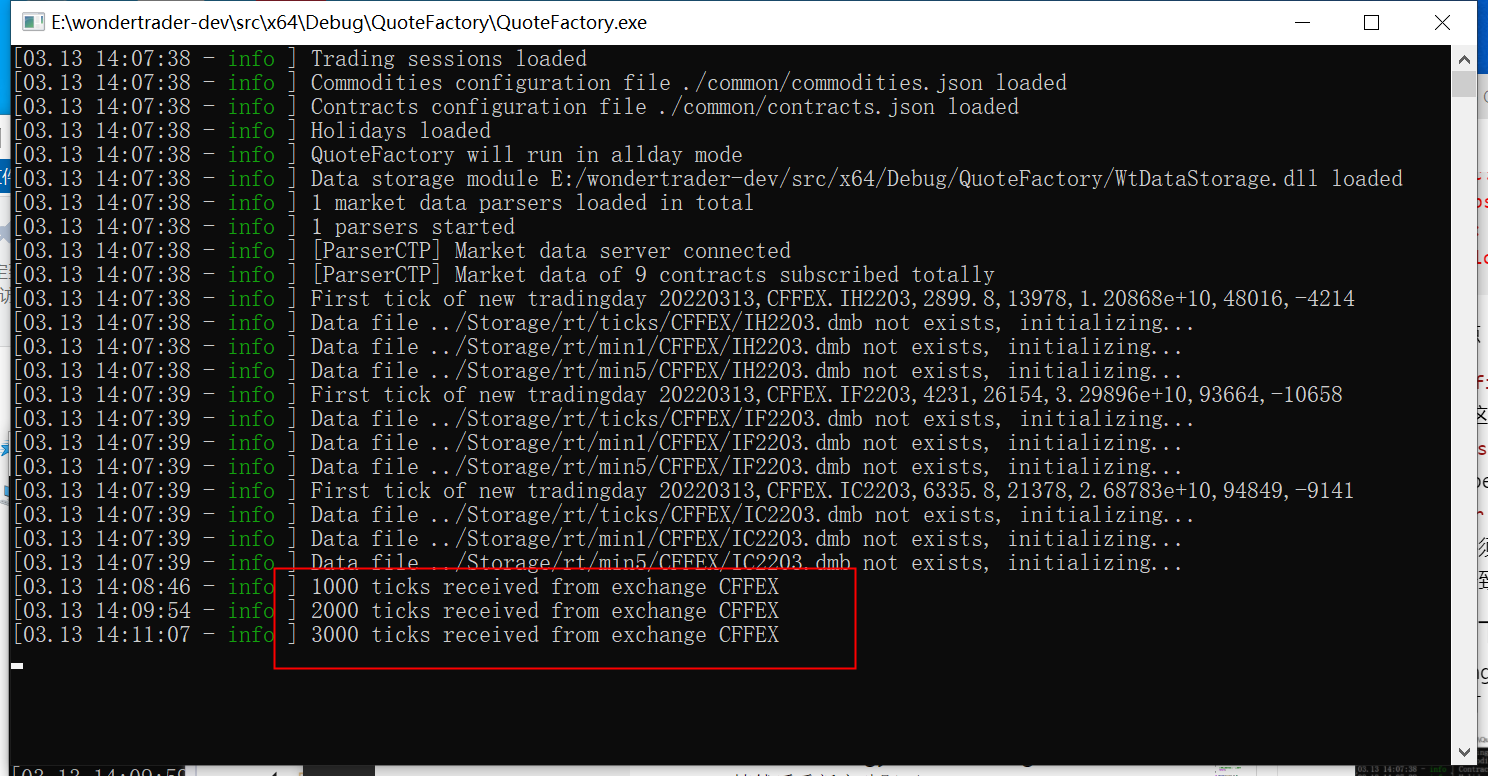

成功截图如下

若出现warning, 则将 "Storage" 文件目录删掉然后重新启动即可

重写CTA策略

为了方便调试, 我对 "WtStraDualThrust" 做了细微改动, 主要是打印回调记录, 源码如下

WtStraDualThrust.h

#pragma once

#include "../Includes/CtaStrategyDefs.h"

class WtStraDualThrust : public CtaStrategy

{

public:

WtStraDualThrust(const char* id);

virtual ~WtStraDualThrust();

public:

virtual const char* getFactName() override;

virtual const char* getName() override;

virtual bool init(WTSVariant* cfg) override;

virtual void on_schedule(ICtaStraCtx* ctx, uint32_t curDate, uint32_t curTime) override;

virtual void on_init(ICtaStraCtx* ctx) override;

virtual void on_tick(ICtaStraCtx* ctx, const char* stdCode, WTSTickData* newTick) override;

virtual void on_bar(ICtaStraCtx* ctx, const char* stdCode, const char* period, WTSBarStruct* newBar) override;

private:

//指标参数

double _k1;

double _k2;

uint32_t _days;

//数据周期

std::string _period;

//K线条数

uint32_t _count;

//合约代码

std::string _code;

bool _isstk;

};

WtStraDualThrust.h

#include "WtStraDualThrust.h"

#include "../Includes/ICtaStraCtx.h"

#include "../Includes/WTSContractInfo.hpp"

#include "../Includes/WTSVariant.hpp"

#include "../Includes/WTSDataDef.hpp"

#include "../Share/decimal.h"

extern const char* FACT_NAME;

//By Wesley @ 2022.01.05

#include "../Share/fmtlib.h"

WtStraDualThrust::WtStraDualThrust(const char* id)

: CtaStrategy(id)

{

}

WtStraDualThrust::~WtStraDualThrust()

{

}

const char* WtStraDualThrust::getFactName()

{

return FACT_NAME;

}

const char* WtStraDualThrust::getName()

{

return "DualThrust";

}

bool WtStraDualThrust::init(WTSVariant* cfg)

{

if (cfg == NULL)

return false;

_days = cfg->getUInt32("days");

_k1 = cfg->getDouble("k1");

_k2 = cfg->getDouble("k2");

_period = cfg->getCString("period");

_count = cfg->getUInt32("count");

_code = cfg->getCString("code");

_isstk = cfg->getBoolean("stock");

return true;

}

void WtStraDualThrust::on_schedule(ICtaStraCtx* ctx, uint32_t curDate, uint32_t curTime)

{

ctx->stra_log_info(fmt::format("回调 on_schedule, date: {}, time: {}", ctx->stra_get_date(), ctx->stra_get_time()).c_str());

// 如果本地无数据, 继续向下执行就会报错

return;

std::string code = _code;

if (_isstk)

code += "-";

WTSKlineSlice *kline = ctx->stra_get_bars(code.c_str(), _period.c_str(), _count, true);

if(kline == NULL)

{

//这里可以输出一些日志

return;

}

if (kline->size() == 0)

{

kline->release();

return;

}

uint32_t trdUnit = 1;

if (_isstk)

trdUnit = 100;

int32_t days = (int32_t)_days;

double hh = kline->maxprice(-days, -2);

double ll = kline->minprice(-days, -2);

WTSValueArray* closes = kline->extractData(KFT_CLOSE);

double hc = closes->maxvalue(-days, -2);

double lc = closes->minvalue(-days, -2);

double curPx = closes->at(-1);

closes->release();///!!!这个释放一定要做

double openPx = kline->at(-1)->open;

double highPx = kline->at(-1)->high;

double lowPx = kline->at(-1)->low;

double upper_bound = openPx + _k1 * (std::max(hh - lc, hc - ll));

double lower_bound = openPx - _k2 * std::max(hh - lc, hc - ll);

WTSCommodityInfo* commInfo = ctx->stra_get_comminfo(_code.c_str());

double curPos = ctx->stra_get_position(_code.c_str()) / trdUnit;

if(decimal::eq(curPos,0))

{

if(highPx >= upper_bound)

{

ctx->stra_enter_long(_code.c_str(), 2 * trdUnit, "DT_EnterLong");

//向上突破

ctx->stra_log_info(fmt::format("向上突破{}>={},多仓进场", highPx, upper_bound).c_str());

}

else if (lowPx <= lower_bound && !_isstk)

{

ctx->stra_enter_short(_code.c_str(), 2 * trdUnit, "DT_EnterShort");

//向下突破

ctx->stra_log_info(fmt::format("向下突破{}<={},空仓进场", lowPx, lower_bound).c_str());

}

}

//else if(curPos > 0)

else if (decimal::gt(curPos, 0))

{

if(lowPx <= lower_bound)

{

//多仓出场

ctx->stra_exit_long(_code.c_str(), 2 * trdUnit, "DT_ExitLong");

ctx->stra_log_info(fmt::format("向下突破{}<={},多仓出场", lowPx, lower_bound).c_str());

}

}

//else if(curPos < 0)

else if (decimal::lt(curPos, 0))

{

if (highPx >= upper_bound && !_isstk)

{

//空仓出场

ctx->stra_exit_short(_code.c_str(), 2 * trdUnit, "DT_ExitShort");

ctx->stra_log_info(fmt::format("向上突破{}>={},空仓出场", highPx, upper_bound).c_str());

}

}

ctx->stra_save_user_data("test", "waht");

//这个释放一定要做

kline->release();

}

void WtStraDualThrust::on_init(ICtaStraCtx* ctx)

{

ctx->stra_log_info(fmt::format("回调 on_init, date: {}, time: {}", ctx->stra_get_date(), ctx->stra_get_time()).c_str());

std::string code = _code;

if (_isstk)

code += "-";

// 获取 CFFEX.IC.2203 的tick数据

WTSTickSlice* ticks = ctx->stra_get_ticks(_code.c_str(), 30);

if (ticks)

ticks->release();

// 获取 CFFEX.IC.2203 的bar数据

WTSKlineSlice *kline1 = ctx->stra_get_bars(code.c_str(), _period.c_str(), _count, true);

if (kline1 == NULL)

{

//这里可以输出一些日志

return;

}

kline1->release();

// 主动订阅 CFFEX.IH.2203 tick数据

ctx->stra_sub_ticks("CFFEX.IH.2203");

}

void WtStraDualThrust::on_tick(ICtaStraCtx* ctx, const char* stdCode, WTSTickData* newTick)

{

//没有什么要处理

ctx->stra_log_info(fmt::format("回调 on_tick, code: {}, date: {}, time: {}", newTick->code(), ctx->stra_get_date(), ctx->stra_get_time()).c_str());

}

void WtStraDualThrust::on_bar(ICtaStraCtx* ctx, const char* stdCode, const char* period, WTSBarStruct* newBar)

{

//没有什么要处理

ctx->stra_log_info(fmt::format("回调 on_bar, code: {}, date: {}, time: {}", stdCode, ctx->stra_get_date(), ctx->stra_get_time()).c_str());

}

- 修改完之后记得重新生成 dll文件并放到 "WtRunner/cta" 目录下

- 确保 "WtRunner/executer" 下有CTA执行器dll文件 "WtExeFact.dll"

CTA策略配置

1."common" 文件夹内容和 "QuoteFactory/common" 保持一致即可

2.actpolicy.yaml

default:

order:

- action: close

limit: 0

- action: open

limit: 0

stockindex:

filters:

- CFFEX.IF

- CFFEX.IC

- CFFEX.IH

order:

- action: closeyestoday

limit: 0

- action: open

limit: 500

- action: closetoday

limit: 0

3.filters.yaml

code_filters:

CFFEX.IF0:

action: ignore

target: 0

strategy_filters:

Q3LS00_if0:

action: ignore

target: 0

4.executers.yaml

# 一个组合可以配置多个执行器,所以executers是一个list

executers:

- active: true #是否启用

id: exec #执行器id,不可重复

trader: tts24 #执行器绑定的交易通道id,如果不存在,无法执行

scale: 1 #数量放大倍数,即该执行器的目标仓位,是组合理论目标仓位的多少倍,可以为小数

policy: #执行单元分配策略,系统根据该策略创建对一个的执行单元

default: #默认策略,根据品种ID设置,如SHFE.rb,如果没有针对品种设置,则使用默认策略

name: WtExeFact.WtMinImpactExeUnit, #执行单元名称

offset: 0, #委托价偏移跳数

expire: 5, #订单超时没秒数

pricemode: 1, #基础价格模式,-1-己方最优,0-最新价,1-对手价

span: 500, #下单时间间隔(tick驱动的)

byrate: false, #是否按对手盘挂单量的比例挂单,配合rate使用

lots: 1, #固定数量

rate: 0 #挂单比例,配合byrate使用

clear: #过期主力自动清理配置

active: false #是否启用

excludes: #排除列表

# - CFFEX.IF

- CFFEX.IC

includes: #包含列表

# - SHFE.au

5.tdparsers.yaml

parsers:

- active: true

bport: 9001

host: 127.0.0.1

id: TTS24

module: ParserUDP

sport: 3997

6.tdtraders.yaml

traders:

- active: true

id: TTS24

module: TraderCTP

ctpmodule: tts_thosttraderapi_se

front: tcp://122.51.136.165:20002

broker: ""

user: ******

pass: ******

appid:

authcode:

quick: true

riskmon:

active: false

policy:

default:

order_times_boundary: 20

order_stat_timespan: 10

cancel_times_boundary: 20

cancel_stat_timespan: 10

cancel_total_limits: 470

7.config.yaml

#基础配置文件

basefiles:

utf-8: true

commodity: ./common/commodities.json #品种列表

contract: ./common/contracts.json #合约列表

holiday: ./common/holidays.json #节假日列表

hot: ./common/hots.json #主力合约映射表

session: ./common/sessions.json #交易时间模板

#数据存储

data:

store:

module: WtDataStorage #模块名

path: ../Storage/ #数据存储根目录

#环境配置

env:

name: cta #引擎名称:cta/hft/sel

product:

session: TTS24 #驱动交易时间模板,TRADING是一个覆盖国内全部交易品种的最大的交易时间模板,从夜盘21点到凌晨1点,再到第二天15:15,详见sessions.json

riskmon: #组合风控设置

active: false #是否开启

module: WtRiskMonFact #风控模块名,会根据平台自动补齐模块前缀和后缀

name: SimpleRiskMon #风控策略名,会自动创建对应的风控策略

#以下为风控指标参数,该风控策略的主要逻辑就是日内和多日的跟踪止损风控,如果回撤超过阈值,则降低仓位

base_amount: 5000000 #组合基础资金,WonderTrader只记录资金的增量,基础资金是用来模拟组合的基本资金用的,和增量相加得到动态权益

basic_ratio: 101 #日内高点百分比,即当日最高动态权益是上一次的101%才会触发跟踪侄止损

calc_span: 5 #计算时间间隔,单位s

inner_day_active: true #日内跟踪止损是否启用

inner_day_fd: 20.0 #日内跟踪止损阈值,即如果收益率从高点回撤20%,则触发风控

multi_day_active: false #多日跟踪止损是否启用

multi_day_fd: 60.0 #多日跟踪止损阈值

risk_scale: 0.3 #风控系数,即组合给执行器的目标仓位,是组合理论仓位的0.3倍,即真实仓位是三成仓

risk_span: 30 #风控触发时间间隔,单位s。因为风控计算很频繁,如果已经触发风控,不需要每次重算都输出风控日志,加一个时间间隔,友好一些

strategies:

cta: # 策略工厂配置

- active: true

id: cta_demo # 策略id

name: WtCtaStraFact.DualThrust # 策略名

params: # 策略参数

code: CFFEX.IC.2203

count: 30

period: m1

days: 30

k1: 0.6

k2: 0.6

stock: false

fees: ./common/fees.json #佣金配置文件

executers: executers.yaml #执行器配置文件

filters: filters.yaml #过滤器配置文件,这个主要是用于盘中不停机干预的

parsers: tdparsers.yaml #行情通达配置文件

traders: tdtraders.yaml #交易通道配置文件

bspolicy: actpolicy.yaml #开平策略配置文件

配置概述

- "tdparsers.yaml", 不在直接从仿真服务器获取数据, 而是本地端口获取数据, 这就是行情落地程序必须打开的直接原因.

- "tdparsers.yaml", 这里不再需要设置

localtime字段. - "config.yaml", 也不在需要

allday字段. - "config.yaml", 中的

strategies/name字段策略名称必须和WtCtaStraFact.cpp中的名称保持一致.

全部配置成功示例如下

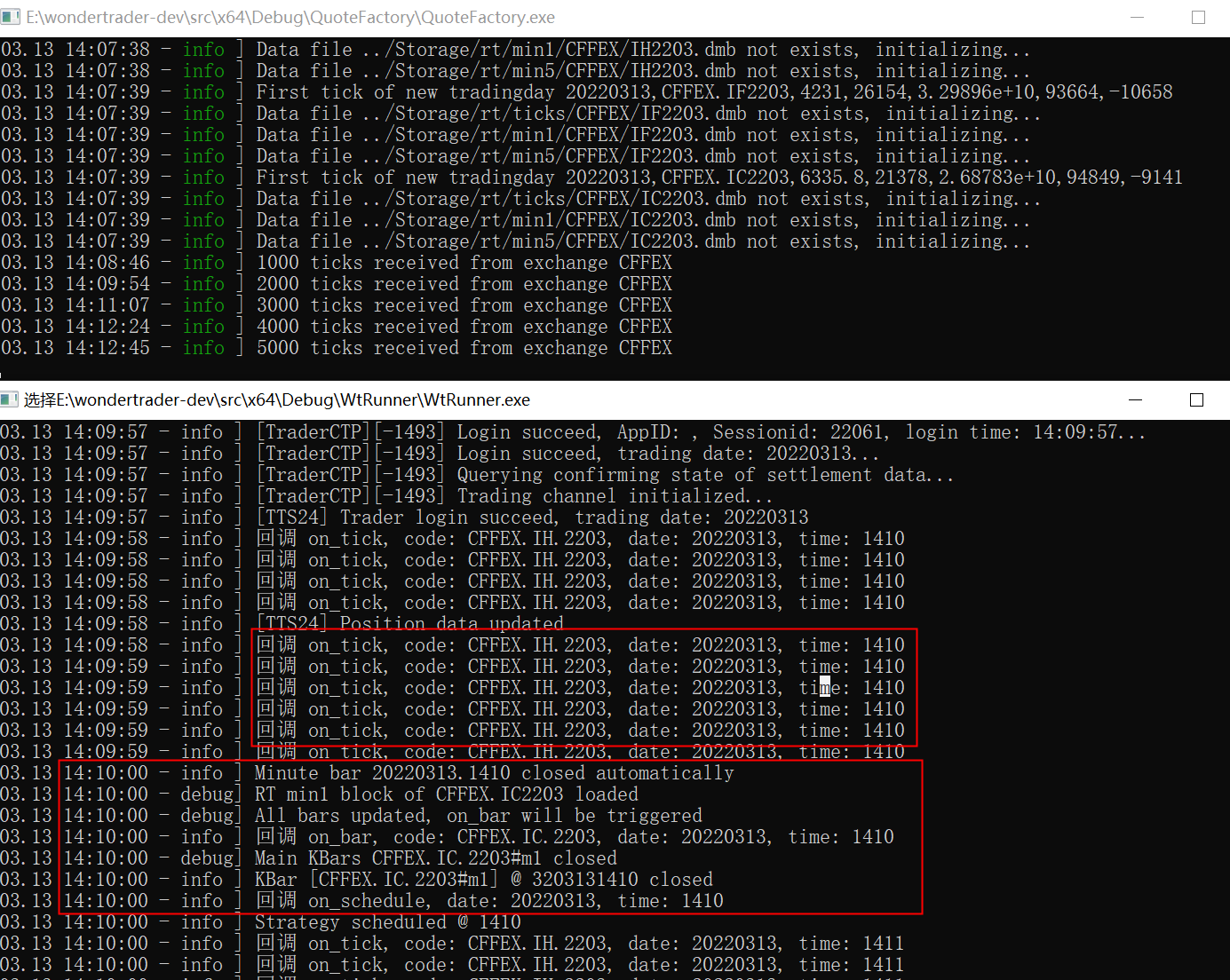

不仅要保证 on_tick 回调成功, 更要保证分钟闭合后 on_schedule 和 on_bar 回调成功